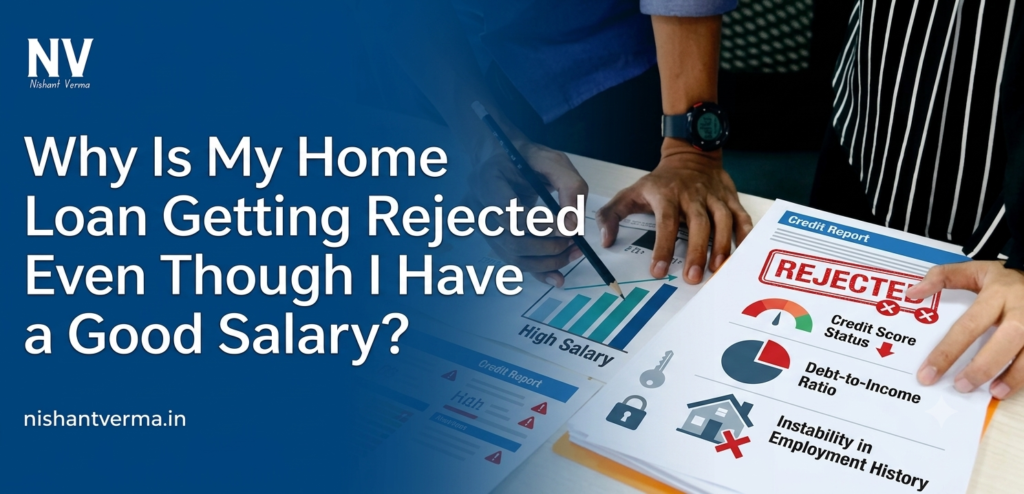

There’s a particular kind of confusion that hits when a bank says no to your home loan application, and your salary slip is sitting right there, perfectly respectable, nothing wrong with it at all. You’ve done everything right. Steady job, decent income, maybe even a promotion last year. And yet the rejection email lands anyway. Quiet, unexplained, almost rude in its brevity.

If you’ve been Googling home loan getting rejected at 1 AM trying to figure out what went wrong, you’re not alone. This happens to salaried professionals far more often than banks like to admit, and the reasons rarely have anything to do with how much you earn.

Why This Actually Matters

A rejected loan application isn’t just a paperwork setback. Every rejection gets logged with credit bureaus, and repeated hard inquiries can quietly drag your credit score down, making the next application even harder to approve. So understanding why your home loan getting rejected situation happened isn’t just about this one property. It affects your entire borrowing future, including car loans, credit cards, even business financing down the line.

What’s Really Going On Here

Banks don’t lend against salary alone. No, that’s not quite right, let me rephrase, they lend against your capacity to repay, which is a very different thing. Think of it like a restaurant checking not just whether you can afford the meal today, but whether you’ll still be a paying customer six months from now without causing trouble.

This capacity gets measured mainly through your credit score and something called the debt-to-income ratio, which is simply how much of your monthly income already goes toward existing debts. A high salary with a high debt-to-income ratio can still trigger home loan getting rejected notices, because the bank sees less breathing room in your finances than the number on your payslip suggests.

How Banks Actually Decide Your Loan Eligibility

- Credit score check: Most Indian lenders want a CIBIL score above 700. Below that, your loan eligibility narrows fast, even with strong income.

- Debt-to-income ratio review: Lenders generally prefer this below 40 to 50 percent. Existing EMIs, credit card dues, even a co-signed loan for a sibling, all count.

- Employment stability check: Frequent job switching, especially within the last year, raises flags regardless of salary.

- Property and legal verification: Sometimes the rejection has nothing to do with you at all. Unclear title documents or disputed property records cause home loans to be rejected too.

- Existing loan history: A missed EMI from three years ago, one you’ve forgotten about, can still sit on your CIBIL score report.

Real-World Examples

Take Rohit, a marketing manager earning 95,000 rupees a month, comfortably above what most banks require for a mid-range home loan. His application still got rejected. Turned out he had two personal loans running simultaneously, pushing his debt-to-income ratio past 55 percent. The bank wasn’t questioning his salary, it was questioning what was left of it after existing obligations.

Or consider Meera, a schoolteacher with a clean repayment history but a credit score sitting at 640 because of one missed credit card payment two years ago. Good salary, poor score, and the mismatch was enough for a home loan getting rejected decision.

Mistakes People Keep Making, And Why

Most applicants assume salary is the whole story. It isn’t. People also underestimate how much unused credit card limits count against their loan eligibility, since banks assume you might max them out. Others apply to multiple banks within days of each other, not realising each hard inquiry chips away at the credit score a little more. There’s no judgment here, this stuff genuinely isn’t taught anywhere.

Pro Tips That Actually Help

Check your CIBIL score report at least two months before applying, not the week before. That gives you time to dispute errors, and errors are more common than people think. Pay down existing EMIs where possible to improve your debt-to-income ratio before submission. Avoid applying to three banks in the same week; pick one, prepare thoroughly, apply once. And if a home loan getting rejected notice does arrive, ask the bank directly for the reason in writing. Most will tell you if you ask properly, they just won’t volunteer it.

Closing Thoughts

A rejected loan feels personal, even when it isn’t. It’s just a system reading numbers the way systems do, without context, without knowing about the medical bill last year or the loan you co-signed for a friend. Fix what’s fixable, understand what isn’t, and try again with clearer eyes. The house isn’t gone, just delayed.

Free Downloadable Resource: A simple pre-application checklist covering credit score checks, document readiness, and debt-to-income calculations is available at the end of this article for readers who want a structured starting point.

Frequently Asked Questions

1. What credit score is needed to avoid home loan rejection?

Most banks look for a CIBIL score of 700 or above. Below 650, approval becomes genuinely difficult regardless of salary.

2. Does a high salary guarantee loan approval?

No. Salary shows earning capacity, but banks weigh it against existing debts, credit history, and the debt-to-income ratio before deciding.

3. Can I reapply immediately after a home loan gets rejected?

It’s better to wait two to three months, fix the underlying issue first, since immediate reapplication often triggers another hard inquiry that lowers your score further.

4. How does debt-to-income ratio affect loan eligibility?

A ratio above 50 percent signals limited repayment capacity to lenders, even when income looks strong on paper.

5. Will checking my own CIBIL score hurt it?

No. A self-check is a soft inquiry and has no negative impact, unlike bank-initiated hard inquiries.

6. What documents reduce chances of home loan rejection?

Clear property title papers, updated income tax returns, and a written explanation for any past credit issues all help significantly.