How do you know if a property is legally safe to buy? The answer often lies in the documents and legal checks most buyers overlook until it’s too late. A friend of mine almost lost eleven lakh rupees on a plot that looked perfect on paper. It had a nice road, a decent view, a seller who smiled a lot. What it didn’t have was a clear title. Nobody told her that until three months after the advance was paid. That’s the thing about real estate. The mistakes are quiet until they aren’t.

This is really the question every buyer eventually asks themselves, usually too late: is this property legally safe to buy, and what documents should I actually check before I hand over my savings? Let’s slow down and go through it properly.

Why This Actually Matters More Than the Price Tag

People obsess over price per square foot. Fair enough, money matters. But a property that isn’t legally safe to buy can cost you far more than a bad negotiation ever would. Disputed titles, unpaid loans on the land, missing approvals… these don’t show up in a nice brochure. They show up later, in court, in a notice slipped under your door, in a bank refusing your home loan because the title isn’t clean.

Understanding this isn’t paranoia. It’s ownership, done properly.

What “Legally Safe” Really Means (Explained Simply)

Here’s a way to think about it. Buying a property without checking its legal status is a little like buying a used car without checking if it’s stolen. It might run fine for years. Or it might get seized the moment someone else shows up with a stronger claim.

A property is considered legally safe to buy when its ownership is clear, its title deed is verifiable, there are no pending loans or court cases attached to it, and every required government approval actually exists, not just promised.

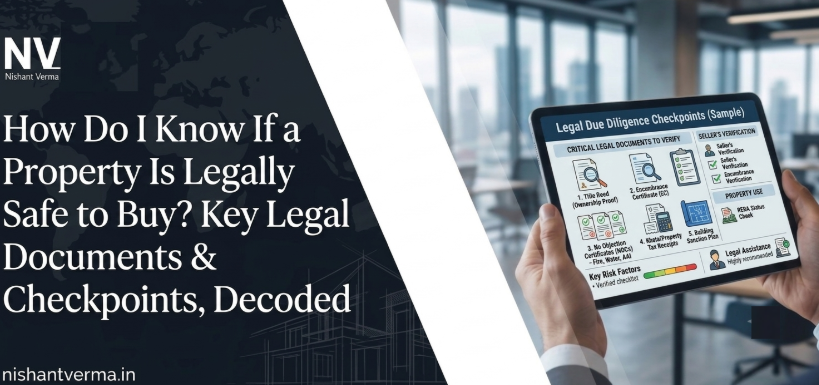

How to Check If a Property Is Legally Safe to Buy, Step by Step

- Verify the title deed. This is the single most important property document. It proves who actually owns the land and whether that ownership can legally be transferred.

- Get an encumbrance certificate. An encumbrance certificate shows whether the property has any existing loans, mortgages, or legal claims against it. No buyer should skip this. Ever.

- Check the sale deed history, going back at least 12 to 15 years if possible, to confirm there’s no broken chain of ownership.

- Confirm the property tax receipts are up to date, and in the seller’s name.

- Look for building or land-use approvals from the local municipal authority. An unapproved structure can be demolished, even years after you’ve moved in.

- Ask for the RERA registration number, if it’s a new project. This alone weeds out a surprising number of shady developers.

Each of these is basic due diligence, and none of them are optional, whatever the seller’s timeline pressure might suggest.

Real-World Examples That Actually Happen

A buyer in Pune once purchased an apartment where the builder had used the same land parcel to secure a construction loan from two different lenders. It surfaced only during resale, five years later. Another case, more common than people admit: a plot sold by one sibling out of three, without the other two ever agreeing to it. The title deed looked fine. The family dispute did not.

These aren’t rare horror stories. They’re Tuesday-afternoon reality for property lawyers.

Mistakes People Keep Making, and Why

Most buyers trust verbally what should be verified on paper. Nobody’s being naive on purpose. It’s just that a smiling seller and a well-lit apartment can quietly override caution. Others assume a bank loan approval means the property is automatically legally safe to buy — it doesn’t. Banks check enough to protect their own money, not necessarily everything a buyer should know.

Pro Tips That Actually Help

Hire an independent property lawyer, not one suggested by the seller or builder. Small cost, real protection. Cross-check the encumbrance certificate with the sub-registrar’s office directly instead of relying only on what’s handed to you. And if a deal feels rushed, that urgency is often the biggest red flag of all.

Closing Thoughts

Buying a home is supposed to feel like an arrival, not a risk. The paperwork isn’t the boring part standing between you and the keys. It is, quietly, the whole point.

FAQs

1. What documents should I check before buying a property?

At minimum, the title deed, encumbrance certificate, latest property tax receipts, building approval, and RERA registration for new projects.

2. How do I know if a property is legally safe to buy?

Verify the ownership chain through the title deed, confirm there are no loans against it via the encumbrance certificate, and check that all municipal approvals exist.

3. What is an encumbrance certificate, and why does it matter?

It’s an official record showing whether a property has any existing loans or legal claims. Without it, you can’t be sure the property is truly free to purchase.

4. Can a bank loan approval guarantee a property is legally safe?

No. Banks verify enough to secure their lending, not everything a buyer should independently confirm.

5. How far back should I check the ownership history?

Most legal experts recommend at least 12 to 15 years of sale deed history to rule out broken ownership chains.

6. Do I need a lawyer to check if a property is legally safe to buy?

It’s strongly recommended. An independent property lawyer catches issues a first-time buyer typically wouldn’t know to look for.